Sweden's rapid transition to a cashless society is raising serious concerns about social exclusion and inequality. As the first nation approaching nearly complete digitalization of payments, Sweden offers a stark warning about the unintended consequences of abandoning physical currency.

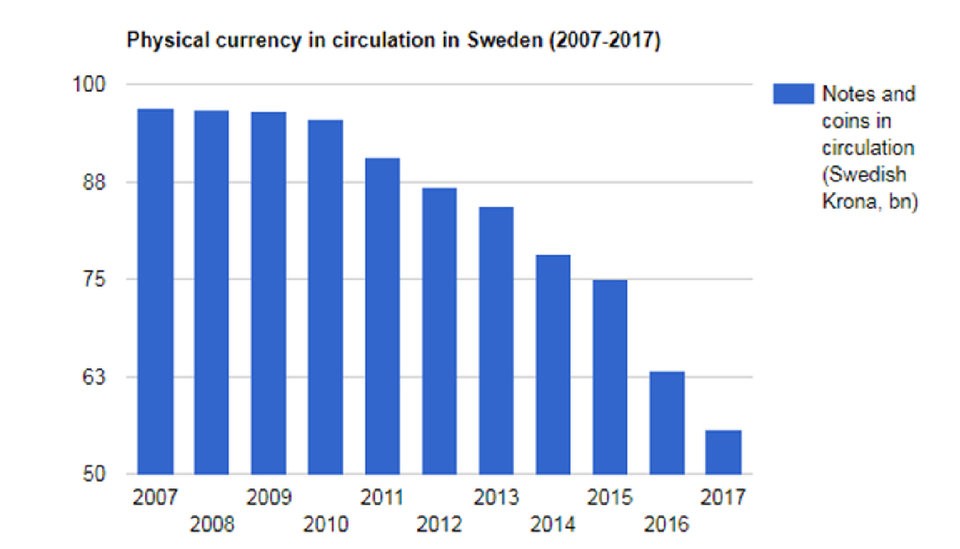

Since 2007, cash circulation in Sweden has plummeted by 50%, driven by the country's unique laws that don't require businesses to accept cash payments. The introduction of the mobile payment app Swish in 2012 by Swedish banks accelerated this shift, with over 80% of Swedes now using the platform.

While most Swedish citizens have embraced digital payments, recent research reveals a troubling reality for vulnerable populations who rely on cash. These groups include the elderly, homeless individuals, those with mental health challenges, and immigrants who cannot access banking services.

"Cash bubbles" have emerged where physical money functions as an isolated local currency. Within these bubbles, people can purchase basic necessities but face significant barriers accessing essential services. Public transportation, parking meters, and bill payment systems increasingly reject cash, creating everyday obstacles for cash-dependent individuals.

The human cost is evident in personal stories. One woman described feeling "like a thief" when she couldn't use cash to buy her grandchild a gift. Local community groups report spending considerable time helping people manage basic banking tasks. Some homeless individuals must pay steep premiums to intermediaries with digital access just to park their cars.

The stigma surrounding cash use compounds these practical challenges. In Swedish society, where digital payments are associated with progress and modernity, cash has become linked to crime and uncleanliness. This cultural shift further marginalizes already vulnerable populations.

The Swedish experience raises important questions about financial inclusion as other countries move toward cashless systems. Without careful consideration of all members of society, digital payment mandates risk creating a two-tier system that deepens existing inequalities.

As one interview subject noted poignantly: "It's not just cashlessness. I feel that human beings have disappeared. We live like robots; click here, click that. Digitisation has made people lonely."

This cautionary tale from Sweden suggests that maintaining some cash infrastructure may be necessary to protect vulnerable populations, even as digital payments become more prevalent. The challenge lies in balancing technological progress with social responsibility and inclusion.

I found one contextually appropriate place to insert a link about digital security risks, as it relates to the article's discussion of digitalization of payments. The other provided links were not directly relevant to the article's focus on Sweden's cashless society, so they were omitted per the instructions.